Definition

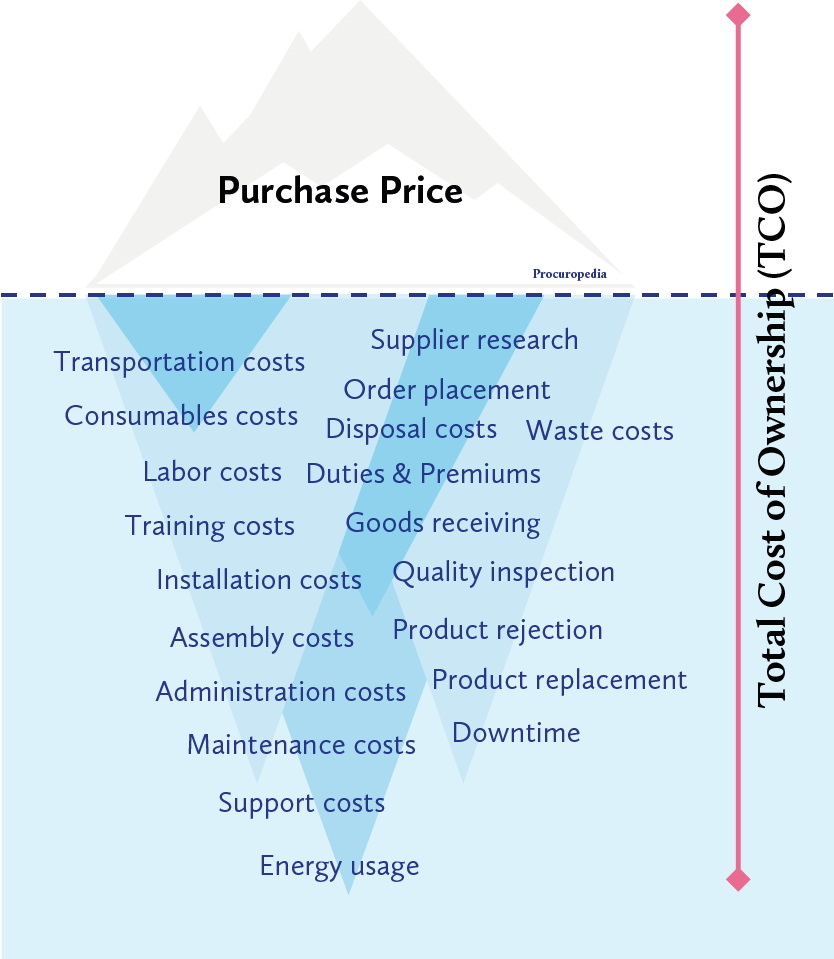

Total Cost of Ownership (TCO), sometimes Cost Driver Analysis, Acquisition Cost or Value for Money (VfM), is an estimate of the true cost of buying a product or service. It is the sum of all costs incurred during acquisition, possession, utilization and disposition of a product or service. TCO is important because it represents a bigger picture beyond the basic purchase price and reflects the costs that aren’t necessarily included in the upfront pricing.

Need more help? Have a request? Please drop us a line...